Summary

- India’s mandatory CSR framework requires eligible companies to deploy 2% of average net profit annually generating a collective CSR budget of over ₹27,000 crore each year

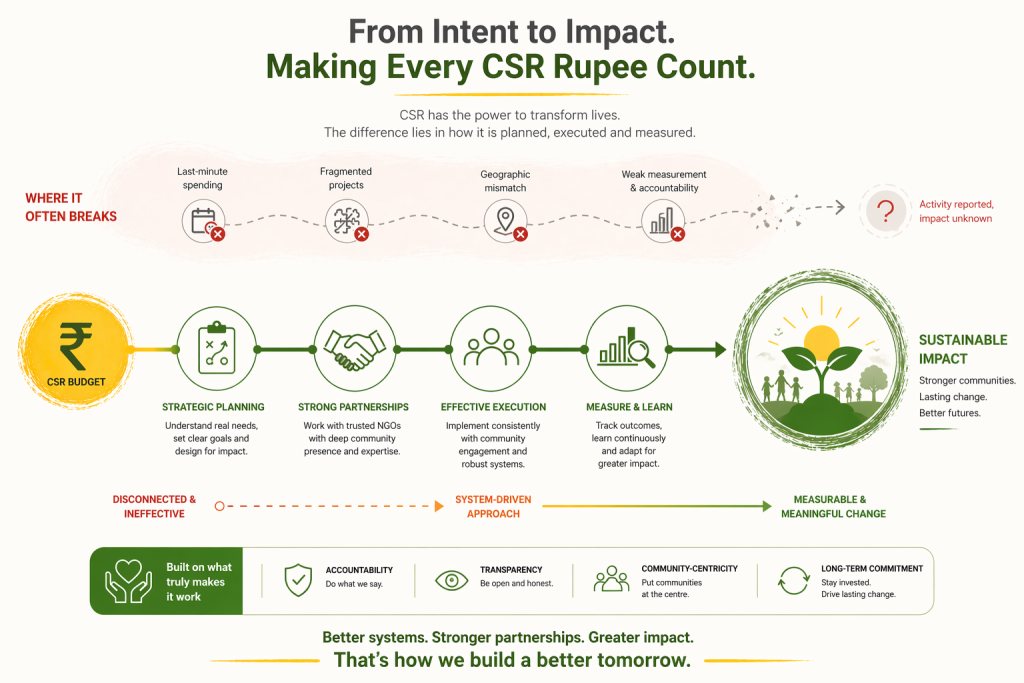

- Despite rising compliance rates, persistent inefficiencies remain — last-minute spending, fragmented project design and weak outcome measurement undermine the impact of significant capital

- Over ₹1,000 crore of allocated CSR funds in the last few financial years went unspent and had to be transferred to designated government funds — a direct consequence of poor planning and insufficient implementation infrastructure

- The most common failure in CSR budget utilisation is not intent but execution — the absence of credible, experienced implementation partners who can absorb funds effectively and deliver measurable outcomes

- NGO partnerships are not a vendor arrangement. They are a systems investment — bringing implementation capacity, community trust, programme design expertise and impact measurement frameworks that companies cannot build in-house

- The strategic shift required is from compliance-driven annual spending to outcome-oriented, multi-year investment aligned with ESG goals and accountable for genuine, verifiable change

The Contradiction at the Heart of Indian CSR

Every year, corporate India commits thousands of crores to social development. The regulatory framework is clear, the compliance machinery is established and the numbers on paper are impressive. India’s collective CSR budget has crossed ₹27,000 crore annually, making it one of the largest pools of directed corporate social investment anywhere in the world.

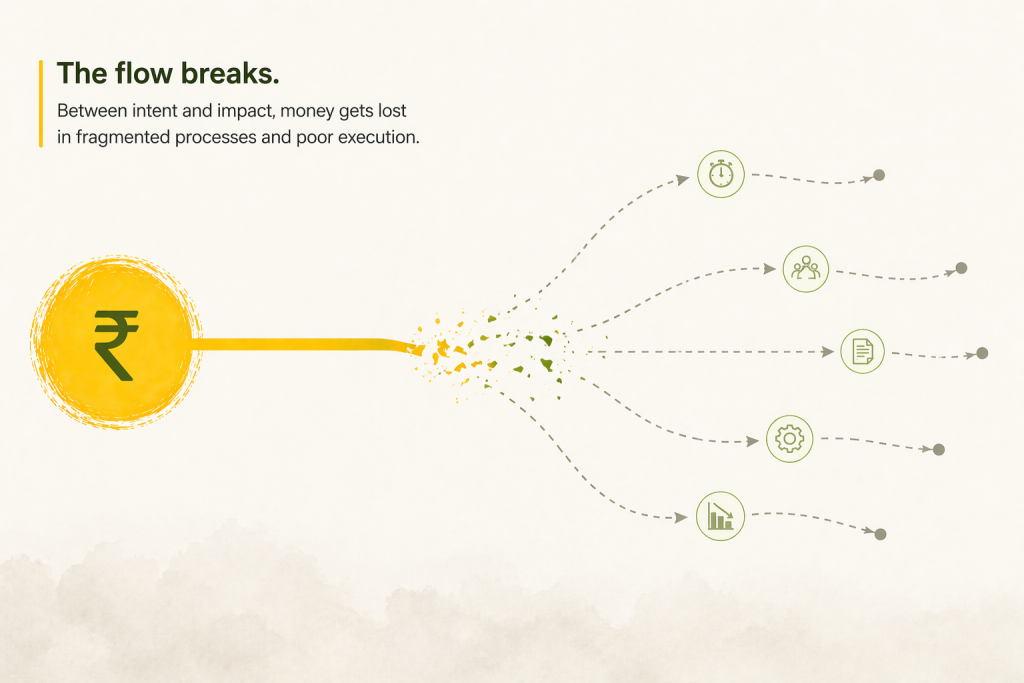

And yet, every year, a significant portion of that budget goes unspent. Another portion is deployed in rushed, poorly designed interventions that produce reports but not results. And a further share funds programmes that are disconnected from the communities they are supposed to serve, the problems they are supposed to solve, and the outcomes that would justify the investment.

The contradiction is stark, and it is worth stating plainly: India has mandated the spend. It has not mandated the impact. And in the gap between those two things — between rupees allocated and lives genuinely changed — lies the central challenge of corporate social responsibility in India today.

This is not primarily a story about bad intentions. Most companies that allocate a CSR budget do so with genuine commitment. It is a story about the difficulty of converting financial resources into systemic change, and about what happens when that difficulty is underestimated, under planned for or addressed with the wrong tools.

The Scale of the CSR Budget in India

Section 135 of the Companies Act 2013 introduced something unprecedented: a legal obligation for profitable companies to invest in social development. Any company with a net worth of ₹500 crore or more, an annual turnover of ₹1,000 crore or more or a net profit of ₹5 crore or more is required to spend at least 2% of its average net profit from the preceding three years on qualifying CSR activities.

The cumulative effect of this mandate has been substantial. Annual CSR spending in India has grown steadily since the law came into force, crossing ₹26,000 crore in FY2021-22 and continuing to rise as corporate profits grow and compliance rates improve. The MCA’s CSR portal now tracks company-level disclosures, making the data more transparent than it has ever been.

Compliance itself has improved significantly. The proportion of eligible companies meeting their full CSR obligation has risen year on year. The framework has created a culture of CSR planning — committees, policies, annual budgets — that did not exist in most companies a decade ago.

But compliance is not impact. And the persistent gap between what the CSR budget is capable of achieving and what it is actually achieving is one of the most important, and least publicly examined, questions in India’s development landscape.

Why Companies Struggle to Spend Their CSR Budget Well

The challenges are real and varied. Understanding them clearly is the first step toward addressing them.

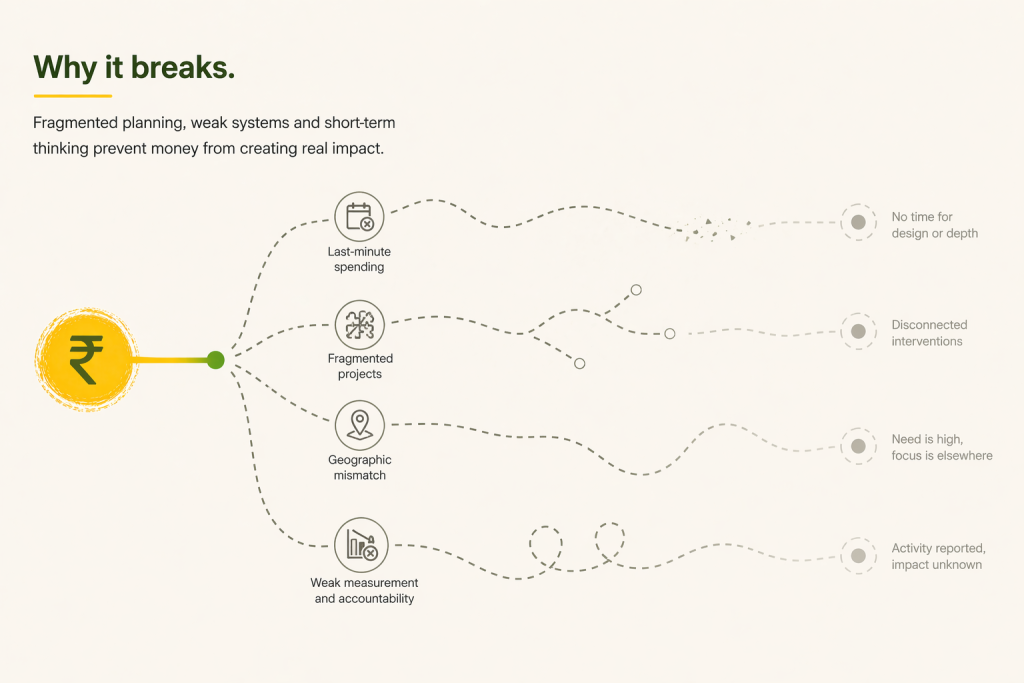

Last-minute compliance pressure

Perhaps the most widespread problem in CSR budget utilisation is the timing of spend. A significant proportion of India’s annual CSR investment is deployed in the final quarter of the financial year, often the final weeks, as companies scramble to meet their obligations before the March 31 deadline.

The consequences of this pattern are predictable. Programmes are selected for speed of deployment rather than quality of design. Implementation partners are engaged without adequate due diligence. Activities are chosen because they are easy to execute and report, not because they address the most significant needs. Year-end CSR spending is, almost by definition, suboptimal CSR spending, and the impact data consistently reflects this.

The root cause is not a lack of funds. It is a lack of planning — the failure to begin programme design early enough in the year to allow for the kind of thoughtful, partner-driven development that effective CSR requires.

Lack of credible implementation partners

Finding NGOs with the scale, governance, programme expertise and geographic reach to absorb significant CSR investment effectively is harder than it sounds. India has hundreds of thousands of registered NGOs, but the proportion with the organisational infrastructure to manage large, multi-year programmes, maintain rigorous monitoring systems and report transparently against outcome indicators is considerably smaller.

Companies that have not invested in building implementation partnerships over time find themselves, when the budget needs to be deployed, choosing between organisations they know little about, under time pressure that prevents adequate assessment. The result is a mismatch between the resources available and the implementation capacity to use them well.

Geographic and operational constraints

Corporate CSR activity is heavily concentrated in the states where company headquarters and major operations are located — Maharashtra, Karnataka, Delhi, Tamil Nadu and Gujarat consistently account for a disproportionate share of total CSR investment. This is partly a function of familiarity and partly a function of implementation infrastructure — NGOs with the capacity to manage significant programmes are more numerous in urban and semi-urban centres than in remote districts.

The consequence is that India’s aspirational districts — the 112 districts identified by NITI Aayog as having the lowest development indicators — receive far less CSR investment per capita than their needs would suggest. The communities that most need the support that a well-deployed CSR budget can provide are, structurally, the communities least likely to receive it.

Fragmented project design

Many companies approach their CSR budget as a portfolio of separate, annual projects rather than as a sustained investment in specific communities and outcomes. A school library in one year, a health camp in the next, a skilling workshop the year after — each may be well-intentioned, but the cumulative effect is fragmentation rather than depth.

Development challenges do not resolve themselves in a single project cycle. Children’s learning outcomes require years of sustained educational support to shift measurably. Community health improvements require sustained access to care, not occasional camps. Women’s economic empowerment requires an ecosystem of skill, finance and market access built over time. CSR budgets deployed in one-year increments, without continuity of intent or implementation, consistently underperform relative to their potential.

Measurement challenges

Most CSR reporting in India measures outputs — the number of people reached, schools built, patients seen, workshops held. These are the numbers that appear in annual reports and MCA filings, and they are the numbers against which CSR teams are most commonly evaluated internally.

What they do not measure is outcomes — whether learning levels improved, whether health indicators changed, whether women’s incomes increased and were sustained. The gap between output measurement and outcome measurement is not merely technical. It represents a fundamentally different understanding of what CSR is for, and companies that measure only outputs are, in effect, measuring whether they spent the budget, not whether spending it made any difference.

The Cost of Inefficient CSR Budget Utilisation

The consequences of poor CSR budget utilisation are not merely reputational, though reputational risk is real in an environment of increasing ESG scrutiny. They are developmental in the most literal sense.

When ₹1,000 crore of CSR funds go unspent in a single year and must be transferred to government funds, that is ₹1,000 crore that did not reach the communities it was intended to serve. When rushed year-end programmes produce activity without impact, the resources consumed could have funded slower, better-designed interventions that would have produced lasting change. When CSR investment is concentrated in areas that are already relatively well-served, the communities with the greatest need continue to go without.

There is also the opportunity cost of misaligned intervention. A health camp that treats symptoms without addressing underlying causes does not build community health resilience. A skilling programme that certifies but does not place does not improve employment. An education programme that builds a computer lab without training teachers to use it does not improve learning outcomes. In each case, the CSR budget has been spent. The problem it was meant to address has not been moved. The needle did not move.

This is not a trivial concern. It is a systemic failure in how one of India’s most significant pools of development capital is being deployed, and it is one that the current framework, focused primarily on ensuring that money is spent rather than that impact is produced, has not yet adequately addressed.

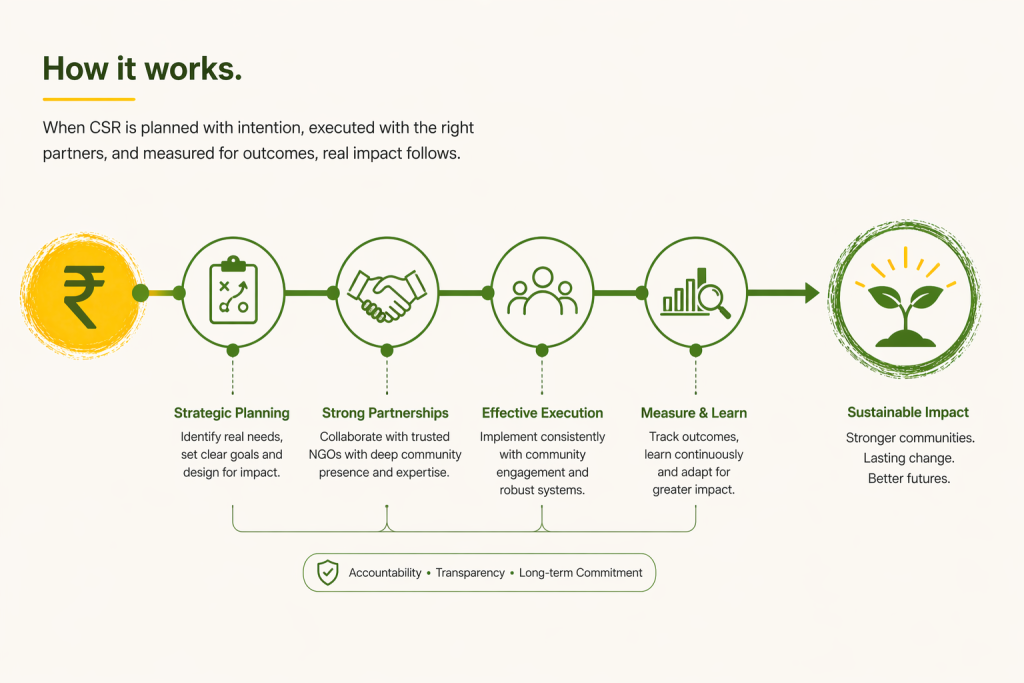

Why NGO Partnerships Solve the CSR Budget Challenge

The organisations best positioned to address the inefficiencies in CSR budget utilisation are not consultancies, not compliance platforms and not government agencies. They are NGOs — specifically, the subset of NGOs that have built the programme design capability, implementation infrastructure, community relationships and measurement systems required to convert financial resources into genuine outcomes.

Strong NGO partnerships address each of the structural challenges described above. They bring programme design expertise that allows CSR budgets to be planned early, against clear theories of change, with realistic timelines and measurable outcome goals. They provide the implementation capacity to deploy funds effectively in the communities and geographies where they are needed, including the aspirational districts that corporate in-house teams cannot easily reach. They offer the community trust and sustained presence that makes multi-year programme continuity possible. And they maintain the monitoring and evaluation frameworks that allow companies to report not just on what was spent but on what changed.

Critically, strong NGO partnerships are not a vendor arrangement. They are a systems investment. When a company commits to a multi-year partnership with an experienced NGO, it is not buying a service. It is investing in an implementation ecosystem — one that compounds in effectiveness over time as community relationships deepen, programme learning accumulates and the evidence base for what works in specific contexts grows stronger.

This is the difference between outsourcing CSR and doing CSR well. Outsourcing says: here is the budget, deliver the activities. Genuine partnership says: here is the budget, here are the outcomes we are committed to achieving together and here is the accountability framework that will tell us both whether we are succeeding.

What Integrated Partnership Looks Like: Smile Foundation

Smile Foundation’s model illustrates what this kind of partnership looks like at scale. Working with over 400 corporate partners across 27 states, the organisation operates across education, healthcare, skilling and women’s empowerment as an integrated development system designed to address the interconnected dimensions of deprivation.

Corporate partners do not simply transfer funds. They co-design programme goals, participate in monitoring and receive outcome-based reporting that allows them to demonstrate to their Boards, their investors, and their regulators not just that the CSR budget was spent, but that it produced verified, meaningful change.

Case Example

A manufacturing company with operations in Rajasthan partnered with Smile Foundation to address the education and health needs of communities near its plant. Over three years, the partnership funded a network of learning centres providing foundational education to over 2,000 children, a mobile health unit conducting regular screenings and referrals and a women’s livelihood programme reaching 500 women in surrounding villages.

By year three, learning outcome assessments showed measurable improvement in literacy and numeracy. Healthcare utilisation in the target communities had increased, with maternal and child health indicators improving. Over 60% of women in the livelihood programme had generated independent income within 18 months.

These outcomes were not the product of a large budget. They were the product of a sustained, integrated, outcome-focused partnership — the kind that only becomes possible when companies plan their CSR budget with the same rigour they bring to their core business investments.

What Companies Should Do Differently

The path from compliance-driven CSR to impact-driven CSR is not complicated. But it requires deliberate choices that many companies have not yet made.

Begin planning the CSR budget at the start of the financial year, not the end. This seems obvious, but the pattern of year-end spending suggests it is not standard practice. Early planning allows for proper partner identification, programme design, baseline data collection and the kind of thoughtful implementation that rushed deployment prevents.

Partner, do not outsource. The distinction matters enormously. A genuine implementation partner is engaged in programme design, shares accountability for outcomes and brings institutional knowledge that improves the quality of the intervention. A vendor delivers activities to specification. The former produces impact. The latter produces reports.

Commit to multi-year programmes. Development outcomes do not materialise in 12 months. Companies that structure their CSR budget as a series of annual projects rather than sustained multi-year investments will consistently find that their spend does not compound into systemic change. Three to five year commitments, with annual reviews against outcome milestones, are the minimum timeframe for serious impact work.

Invest in measurement from the beginning. Outcome measurement is not something to layer onto a programme after it is designed. It requires baseline data, clear outcome indicators and monitoring systems built into the programme architecture from the start. Companies that invest in measurement are companies that can learn from their CSR investment — and that learning is itself a form of value.

Align CSR with business strengths. The most effective corporate CSR programmes are those where the company’s core competencies — in technology, logistics, healthcare, finance, agriculture — are brought to bear on the development challenges being addressed. A pharmaceutical company funding community health programmes is not just providing money. It is potentially bringing scientific knowledge, supply chain capacity and institutional expertise that a pure financial grant cannot replicate.

The Shift Ahead: From Spending to Impact

The regulatory direction in India is clear. ESG integration, outcome-based reporting expectations and the increasing scrutiny of institutional investors are all pushing corporate CSR from a compliance function toward a strategic one. The companies that will be best positioned in this environment are not those that have the largest CSR budgets. They are those that can demonstrate, with credible evidence, that their CSR investment is producing genuine, measurable change.

This shift requires a different relationship with the CSR budget — not as an annual obligation to be discharged, but as a strategic resource to be deployed with the same rigour and accountability that companies bring to their core capital allocation decisions. It requires a different relationship with implementation partners as systems builders to be invested in over time. And it requires a different definition of success — not the clean deployment of a budget, but the verified improvement of lives.

The Budget Is Not the Challenge

India’s CSR framework has achieved something significant: it has created a culture of corporate social investment where none existed before, channelled tens of thousands of crores toward social development, and established accountability mechanisms that are slowly but genuinely improving.

But the next phase of CSR in India will not be defined by the size of the CSR budget. It will be defined by what happens to it — by whether the resources that corporate India is legally required, and increasingly morally committed, to invest in social development are deployed in ways that produce outcomes commensurate with their scale.

The challenge is not spending the CSR budget. Every eligible company in India is capable of that. The challenge is spending it in ways that make a difference that can be verified, that lasts beyond the programme cycle, and that justifies the investment in the lives of the people it is intended to serve.

That challenge is solvable. But it requires planning, partnership, patience, and a willingness to be held accountable for outcomes rather than only activities. For the companies ready to make that commitment, the opportunity — to contribute meaningfully to India’s development while building genuine ESG credibility — has never been greater.

Frequently Asked Questions

What is a CSR budget?

A CSR budget is the amount of money a company is required or chooses to allocate for corporate social responsibility activities. Under India’s Companies Act 2013, eligible companies must spend at least 2% of their average net profit from the preceding three financial years on qualifying CSR activities each year. The CSR budget must be planned, deployed on eligible activities, and reported publicly through the MCA portal.

What happens if CSR funds are unspent?

If a company does not spend its full CSR budget in a financial year, the unspent amount must be transferred to a designated Unspent CSR Account within 30 days of the financial year end. Funds related to ongoing projects must be spent within three years. Funds not linked to ongoing projects must be transferred to a Schedule VII government fund within six months. Non-compliance can result in penalties of up to three times the unspent amount.

How can companies use their CSR budget more effectively?

The most effective approach combines early planning, strong implementation partnerships, multi-year programme commitments and outcome-based measurement. Companies that begin programme design at the start of the financial year — rather than the end — and that partner with experienced NGOs rather than rushing to deploy funds under deadline pressure, consistently achieve stronger and more verifiable outcomes from their CSR investment.

Why should companies partner with NGOs for CSR implementation?

NGOs with established programme design capability, community presence, and monitoring systems provide the implementation infrastructure that most companies cannot build in-house. They enable last-mile reach into communities and geographies that corporate teams cannot easily access, bring sustained community relationships that make multi-year programmes possible, and offer the impact measurement frameworks that regulators and investors increasingly require.

What activities are eligible under the CSR budget?

Eligible CSR activities are defined in Schedule VII of the Companies Act and include education, healthcare, hunger and poverty alleviation, environmental sustainability, women’s empowerment, rural development, skilling and contributions to specified government funds. Activities that benefit only company employees, involve political contributions, or are conducted outside India do not qualify. All activities must align with the company’s Board-approved CSR policy.

How is CSR impact measured?

CSR impact measurement involves tracking both outputs — activities delivered, people reached — and outcomes — actual changes in learning levels, health indicators, income or other development metrics. Strong impact measurement requires baseline data, clear outcome indicators established before programme implementation, regular monitoring and ideally third-party verification. India’s regulatory framework is moving toward mandatory outcome reporting for larger CSR programmes.

What are the most common mistakes in CSR budget planning?

The most common mistakes are leaving programme planning until late in the financial year, selecting implementation partners under time pressure without adequate due diligence, designing one-off projects rather than sustained multi-year programmes, measuring outputs rather than outcomes and concentrating investment in geographically convenient areas rather than communities with the greatest need. Each of these patterns is addressable through earlier, more deliberate planning and stronger implementation partnerships.

How does Smile Foundation help companies deploy their CSR budget effectively?

Smile Foundation works with corporate partners to co-design programmes aligned with specific development goals, implement them across 27 states through its established community and implementation networks, monitor outcomes rigorously through regular assessments and report transparently against agreed indicators. The organisation’s integrated model spanning education, healthcare, skilling and women’s empowerment allows corporate partners to address the interconnected dimensions of development challenges through a single, accountable implementation relationship.

Can CSR funds be used for multi-year programmes?

Yes, and multi-year programmes are increasingly encouraged under the CSR framework. The rules create a specific mechanism for ongoing projects, allowing unspent funds allocated to these projects to be held in the Unspent CSR Account and deployed over up to three years. This structure directly incentivises the kind of sustained, multi-year engagement that produces stronger outcomes than annual project cycles.

How should companies align their CSR budget with ESG goals?

CSR and ESG are increasingly integrated in how regulators, investors and civil society assess corporate social performance. Companies should ensure that their CSR budget is allocated to programmes that contribute to clearly defined social and environmental outcomes, reported against standardised metrics and verified through credible third-party assessments. Aligning CSR spend with specific SDGs and tracking progress against those goals provides the framework that most institutional ESG assessments are looking for.